Today, the U.S. Department of the Treasury announced that it will begin the orderly wind down of its remaining portfolio of $142 billion in agency-guaranteed mortgage-backed securities (MBS).

Excerpts from the Presser...

Starting this month,Treasury plans to sell up to $10 billion in agency-guaranteed MBS per month, subject to market conditions. At the end of each month, Treasury will post on its website the total agency-guaranteed MBS sales it has made, broken down by coupon and agency.

“We’re continuing to wind down the emergency programs that were put in place in 2008 and 2009 to help restore market stability, and the sale of these securities is consistent with that effort,” said Mary J. Miller, Assistant Secretary for Financial Markets. “We will exit this investment at a gradual and orderly pace to maximize the recovery of taxpayer dollars and help protect the process of repair of the housing finance market.”

The following frequently asked questions provide further information regarding Treasury’s plan to wind down its $142 billion portfolio of agency-guaranteed mortgage-backed securities (MBS) at a gradual and orderly pace. Starting this month, Treasury plans to sell up to $10 billion in agency-guaranteed MBS per month, subject to market conditions.

General

Why does Treasury hold a portfolio of agency-guaranteed MBS?

The Housing and Economic Recovery Act of 2008 (HERA) gave Treasury the authority to purchase agency-guaranteed MBS to provide stability to financial markets, prevent disruption in the availability of mortgage finance, and protect taxpayers. Treasury’s actions helped stabilize the mortgage market at a time of unprecedented market volatility and illiquidity. Treasury purchased agency-guaranteed MBS between October 2008 and December 2009. As of March 15, the current market value of Treasury’s holdings is approximately $142 billion.

Why is Treasury winding down its MBS portfolio?

Selling MBS is consistent with the general pattern of Treasury divestment of financial assets acquired during 2008 and 2009 as part of the various financial stabilization programs. Aided by such programs, today, the market for agency-guaranteed MBS has notably improved along with broader financial conditions since Treasury acquired the portfolio. Additionally, Treasury’s mission does not typically include managing a large mortgage portfolio.

When will the selling commence?

Treasury will begin to gradually wind down its MBS portfolio starting this month.

Over what time frame will the unwind take place?

Treasury plans to sell up to $10 billion of securities per month, subject to market conditions. This is in addition to principal payments (currently ranging between $3 and $5 billion per month). If the sales proceeded at the full $10 billion per month, the portfolio would be unwound in whole over approximately one year, depending on future rates of prepayments. If market conditions change and Treasury slows asset sales, it is possible that the unwind will take a longer period of time.

Once started, would Treasury consider suspending the sale of its MBS portfolio?

Selling the MBS portfolio is subject to market conditions. There is not a rigid set of criteria that will be used to suspend selling. Evidence of adverse market conditions could lead to a change in the sales frequency of the program. Treasury will constantly monitor the market, and if market conditions become less favorable, the sales could be suspended.

What impact will this program have on primary mortgage rates?

We believe that this portfolio can be sold with minimal impact on the market and a minimal impact on primary mortgage rates.

Under what authority is Treasury winding down its MBS portfolio?

The Housing and Economic Recovery Act of 2008 (HERA) gave Treasury the authority to sell holdings acquired under that act.

What implications will this approach have for Treasury debt issuance?

The sale of these securities will allow Treasury to borrow less in 2011 and 2012, but will not alter Treasury’s previously stated debt management objectives.

Is this action related to the debt limit?

No. This action is consistent with a general pattern of Treasury continued divestment of assets acquired during 2008 and 2009 as part of the various financial stabilization programs. Additionally, the projected pace of sales, $10 billion per month, will not meaningfully extend the expected time until Treasury will reach the debt limit.

Relationship to Housing Finance Reform and Fannie Mae and Freddie Mac (The “Enterprises”)

How does this announcement relate to the broader objectives of housing finance reform?

This action is independent from housing finance reform and is a part of the Administration’s broader efforts to wind down the emergency financial stabilization programs that were put in place in 2008 and 2009.

Will this announcement impact current administration policy regarding the wind down of the agency-guaranteed MBS held in the Enterprises’ portfolios?

No. The Enterprises are currently in the process of gradually reducing the size of their retained portfolios at a pace of no less than 10 percent per year, as they agreed to do in the preferred stock purchase agreements between the Treasury and the Enterprises. Both Enterprises are on track to meet or exceed the scheduled reductions, and the Administration does not anticipate any changes to this policy.

Will this announcement impact the Administration’s commitment to supporting the Enterprises’ obligations?

No. The government is committed to ensuring that Fannie Mae and Freddie Mac have sufficient capital to perform under any guarantees issued now or in the future and the ability to meet their debt obligations.

Execution Details

What types of MBS will be sold?

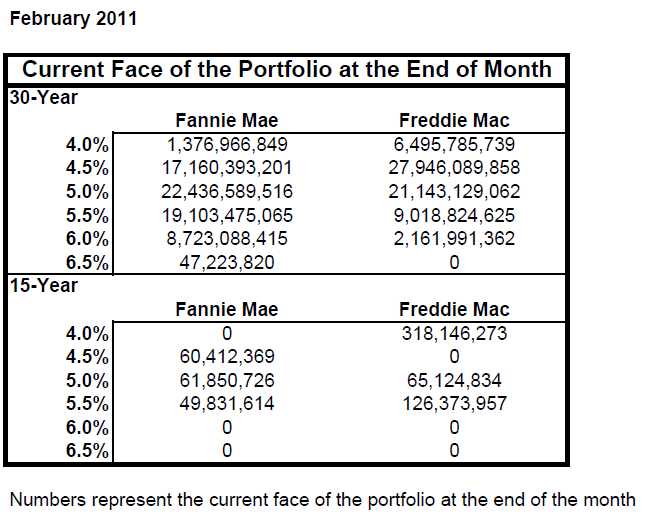

Treasury intends to sell all of its agency-guaranteed MBS holdings. Treasury’s portfolio consists primarily of 30-year fixed-rate MBS that are guaranteed by either Fannie Mae or Freddie Mac. There is also a smaller amount of 15-year fixed-rate MBS guaranteed by Fannie Mae and Freddie Mac, and one 10/20 MBS guaranteed by Fannie Mae. A complete list of the total MBS holdings by coupon and agency is available on the Treasury website at:

What will be the frequency of the sales?

There will be no pre-scheduled times and sizes of individual trades. Treasury will sell up to $10 billion per month, subject to market conditions. Sales of MBS out of the portfolio can occur daily.

How will you decide which securities to sell at any given time?

Treasury will monitor supply and demand dynamics in the market and determine the optimal timing for the sale of securities. Decisions to sell bonds will be based on both quantitative and qualitative market metrics. Treasury will also consider the composition of its portfolio holdings as well as indications of interest from eligible counterparties when determining security selection. State Street Global Advisors (SSgA) is the manager for Treasury’s portfolio and will assist in this analysis.

Will reverse inquiries be allowed?

Treasury will ensure a competitive bidding process that maximizes value for the taxpayer. Dealers are encouraged to show interest in specific trades or securities, but trades will be executed competitively.

Will these trades be specified pool trades or executed as “To-Be Announced” (TBA) trades?

Many of the securities in Treasury’s portfolio currently have a market value higher than TBA prices. As such, these securities will be traded as specified pools. Those securities that do not have a market value higher then TBA prices may be executed as TBA transactions.

Will the Treasury engage in coupon swaps and dollar rolls?

No. All transactions will be outright sales, as authorized by HERA.

Will you consider structuring Collateralized Mortgage Obligations (CMOs) as part of the unwind strategy?

No. Bonds will be sold as they were initially purchased without any additional structuring.

When will the trades settle?

Most trades will settle at monthly intervals on the regularly scheduled TBA settlement days. It is possible to settle trades on different days. Trades settling away from regularly scheduled TBA settlement days would only occur if they were in the taxpayers’ best interest.

Who will settle trades?

SSgA, as financial agent for the Treasury, will be responsible for facilitating the settlement of all sales in the portfolio.

Is the Treasury planning to reinvest the proceeds in any other assets?

No. As mandated under HERA and the Dodd-Frank Act, the proceeds from the MBS sales will be deposited in the General Fund of the Treasury.

Transparency

How will Treasury disclose completed sales?

Consistent with current practice, at the end of each month Treasury will post its portfolio holdings, including any sales that were completed, broken down by coupon and agency. That posting will be available on the Treasury website at: http://www.treasury.gov/resource-center/data-chart-center/Pages/mbs-purchase-program.aspx

Will Treasury post the exact CUSIPs that they own?

No. Given the Treasury’s approach to MBS sales, providing CUSIP level data could reduce the ability to efficiently execute sales.

Will Treasury provide a schedule in advance that displays the list of securities they intend to sell and times of transactions?

No. Treasury will retain flexibility to adjust to supply and demand conditions for specific issues and adjust its wind down strategy accordingly. This will provide the greatest opportunity to ensure best execution for the taxpayer through competitive sales.

Will you publish the counterparties in each MBS trade?

No. Treasury will not publish dealer market shares or specific trade details. Doing so would decrease the ability of Treasury to maximize value for taxpayers.

External Money Managers

Why is it necessary for the Treasury to transact through an external investment manager?

The operational characteristics of MBS purchases and sales are complex and external managers have an ability to execute and manage efficiently while, at the same time, minimizing operational and financial risks.

Treasury is not well positioned to actively trade mortgage-backed securities in the market on a day-to-day basis. External investment managers are used to ensure best execution in the market and maximize value for taxpayers.

How was SSgA selected?

SSgA was selected as part of a competitive process at the outset of the Treasury program to acquire, manage and dispose of MBS. Initially, Treasury hired both Barclays Global Investors (BGI) and SSgA. At the end of 2009, when Treasury completed its MBS purchases, administration of the program was consolidated and it is now managed solely by SSgA..

Is Treasury hiring other money managers to assist with security selection and execution strategy?

Yes. Smith, Graham, and Company Investment Advisors (Smith Graham) will provide additional assistance with the security selection process. On a weekly basis, Smith Graham will provide analytical support to Treasury.

Is Treasury considering hiring other money managers to assist with execution of the sales of MBS?

No. Adding additional managers would increase complexity and add to our operational risk. Intensive coordination and additional surveillance would be required to ensure that multiple independent managers did not work at cross purposes in the market. Using a single manager offers the best approach to optimizing the sale of the portfolio and protecting the taxpayers’ best interests.

How will Treasury ensure that SSgA is making prudent decisions on behalf of taxpayers?

In its agreement with Treasury, SSgA has a mandate to protect taxpayers and maximize value through best execution. Treasury will monitor SSgA and receive regular feedback regarding security selection, timing, and general market conditions to ensure that SSgA is fulfilling its obligations to taxpayers. Additionally, other divisions at SSgA will not be allowed to buy securities directly from Treasury’s portfolio.

What measures will Treasury take to ensure that SSgA will not have in unfair advantage relative to other market participants due to the information it receives?

A wall exists at SSgA that appropriately segregates the investment management team that implements the Treasury’s agency MBS program from other advisory trading activities of the firm. When Treasury hired SSgA, SSgA built a team that is focused exclusively on managing Treasury’s portfolio that is separate from the rest of the firm. Treasury monitors compliance with the requirement to maintain the wall.

Who will SSgA trade with?

SSgA will trade with dealers who meet SSgA’s counterparty credit requirements. Dealers may submit bids for themselves or on behalf of their clients.

Will SSgA be required to spread their business between dealers?

There are no pre-set market share targets for dealers. SSgA will ensure competition between dealers that maximizes best execution for the taxpayer. SSgA will also ensure diversity among the dealers. Treasury will constantly monitor the dealer selection process to ensure that no dealers or market participants are provided an unfair advantage.

FREQUENTLY ASKED QUESTIONS ON TREASURY’S PLAN TO SELL MBS

A few comments...

Treasury did not set a floor on how much MBS they can sell in a given month, but they did set a ceiling at $10 billion. If investor demand warrants, expect Treasury to offer $10 billion a month. If MBS valuations (yield spreads) weaken significantly as Treasury tries to sell, they will back off and let spreads stabilize before resuming operations. We don't expect that to happen unless benchmark yields rise substantially because, for example, the Fed hinted at a rate hike (4.5s would fall off a ledge). If necessary Treasury could halt this program all together, but $10 billion a month only adds $2.5 billion in loan supply per week. When you consider how slow a year it's been for new production MBS, we don't think it'll cause a major disruption.

In terms of timing, it would behoove Treasury to sell their lowest coupons first, especially if Treasury thinks rates will rise in the year ahead. At the moment Treasury is holding mostly 4.5 30-year coupons ($45 billion). With TBA supply very muted at the moment, we don't see many barriers that might prevent Treasury from selling the full $10 billion per month. If rates do drop substantially and the MBS market moves "Down in Coupon", Treasury may run into a barrier as investors look to avoid MBS coupons with heightened prepayment risk like 5.0s and 5.5s. Then again the street has been burned repeatedly over the past year by automatically assuming lower mortgage rates would equal a big jump in prepayment speeds. It just didn't happen. Qualifying for a loan isn't as simple as it used to be...one 30-day late is enough to kill a deal these days. Plus in the past, when prepayment speeds did pick up, investors looked for protection in the specified pool mortgage market. These MBS are backed by loans that have demonstrated a consistent performance (have a pay history). Generally MBS investors are willing to "pay-up" (pay more) to get their mitts on this paper. A large portion of Treasury's MBS holdings will be sold as specified "pay-ups". So even if rates do decline, there should still be demand for Treasury's holdings. (5.0 MBS coupons for example have already entered a "burnout" phase where lower rates will have little impact on prepayment speeds).

Plain and Simple: We don't see this causing a major disturbance in the TBA MBS market. The general direction of benchmark rates will largely dictate the direction of mortgage rates. We don't think this is a hint of things to come from the Fed either. When the Fed is ready to finally start selling their MBS holdings, the market will have already pushed rates higher and the market for their holdings would be weak because the coupons on their balance sheet would be trading at a sizeable discount. Thus the Fed will likely be forced to hold onto a large portion of their MBS portfolio to avoid shocking the market with too much duration.

The mortgage market was caught off-guard by this news though. Consequently there has been a knee-jerk reaction wider in current coupon MBS spreads and lower in current coupon MBS prices. That move has already started correcting though...

by Adam Quinones Mortgage News Daily March 21, 2011

Treasury to Sell MBS Holdings. Minimal Shock Expected